Marvelous Impairment Loss Journal Entry Best Balance Sheet Companies

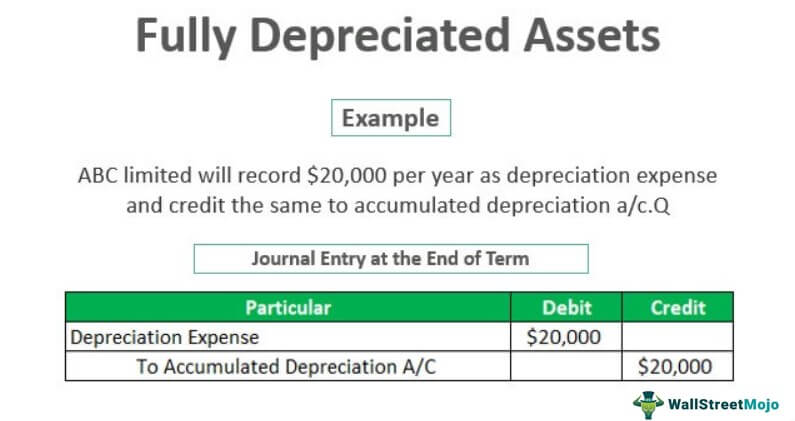

Fully Depreciated Assets Definition Examples How To Account

Find out impairment loss if. If the implied goodwill is higher than goodwill allocated there is no goodwill impairment. Allowance Methodrequires the use of valuation account for the receivables. The higher of fair value less costs of disposal and value in use. Fixed asset impairment journal entry Overview. If that asset is impaired beyond repair and is just junk you get rid of it by this journal entry. Now your post asks about the reversal of a previous impairment lets say the reversal is for 900. With the exception of goodwill and certain intangible assets for which an annual impairment test is required entities are required to conduct impairment tests where there is an indication of impairment of an asset and. Impairment loss is recognized immediately in PL unless the asset is carried at revalued amount Thus entries would be. Key Terms accrue.

In each case the write down of inventory journal entries show the debit and credit account together with a brief narrative.

The journal entry to record impairment is straightforward. Fixed asset impairment journal entry Overview. FASB defines impairment loss as the amount by which the carrying value exceeds an assets fair value. Loss on Impairment Abandonment whatever you want to call it If there is some scrap value to the equipment you should make this journal entry. Dr Profit or Loss Account 2000 Cr Asset Account 2000. The higher of fair value less costs of disposal and value in use.

Impairment loss is recognized immediately in PL unless the asset is carried at revalued amount Thus entries would be. Dr Impairment losses ac PL account Cr Asset account ac Balance sheet account. As mentioned above the higher the assets net realizable value and its value in use. If the implied goodwill is higher than goodwill allocated there is no goodwill impairment. Dr Asset Account 900 Cr. However before recording the impairment loss a company must first determine the recoverable value of the asset. Now your post asks about the reversal of a previous impairment lets say the reversal is for 900. Carrying amount Book value of the assets in the accounting records. FASB defines impairment loss as the amount by which the carrying value exceeds an assets fair value. To increase to augment.

FASB defines impairment loss as the amount by which the carrying value exceeds an assets fair value. We simply undo the previous impairment entry. An impairment loss is recognized through a journal entry that debits Loss on Impairment debits the assets Accumulated Depreciation and credits the Asset to reflect its new lower value. Impairment loss Carrying amount - Recoverable amount. Find out impairment loss if. Loss on Impairment Abandonment whatever you want to call it If there is some scrap value to the equipment you should make this journal entry. Impairment losses on receivables are charged to other operating expenses or financial expenses debit entry - depending on the type of claims covered by the allowance. If it had not previously been the subject of a revaluation and is now simply the subject of an impairment of 2000 the entry would be. To be added as increase profit or damage especially as the produce of money lent. Only create this entry if the value of a designated asset is not expected to recover.

To increase to augment. As mentioned above the higher the assets net realizable value and its value in use. An impairment loss is recognized through a journal entry that debits Loss on Impairment debits the assets Accumulated Depreciation and credits the Asset to reflect its new lower value. To recognize impairment on accounts receivable. If the implied goodwill is higher than goodwill allocated there is no goodwill impairment. Carrying amount Book value of the assets in the accounting records. Loss on Impairment Abandonment whatever you want to call it If there is some scrap value to the equipment you should make this journal entry. The journal entry to record impairment is straightforward. An impairment loss happens when the value of a fixed asset abruptly falls below its carrying cost. With the exception of goodwill and certain intangible assets for which an annual impairment test is required entities are required to conduct impairment tests where there is an indication of impairment of an asset and.

We simply undo the previous impairment entry. Impairment loss is recognized immediately in PL unless the asset is carried at revalued amount Thus entries would be. To recognize impairment on accounts receivable. The higher of fair value less costs of disposal and value in use. In each case the write down of inventory journal entries show the debit and credit account together with a brief narrative. Dr Asset Account 900 Cr. To arise or spring as a growth or result. A carrying amount is not recoverable if it is greater than the sum of the undiscounted cash flows expected from the assets use and eventual disposal. Find out impairment loss if. The corresponding entry credit entry is posted to your account Impairment of receivables in analytical account of the counterparty.

To come to by way of increase. Dr Asset Account 900 Cr. The journal entry to record an impairment is a debit to a loss or expense account and a credit to the related asset. The corresponding entry credit entry is posted to your account Impairment of receivables in analytical account of the counterparty. We simply undo the previous impairment entry. An impairment loss is recognized through a journal entry that debits Loss on Impairment debits the assets Accumulated Depreciation and credits the Asset to reflect its new lower value. To be added as increase profit or damage especially as the produce of money lent. The general ledger accountant enters the requested journal entry in the general ledger. However before recording the impairment loss a company must first determine the recoverable value of the asset. The higher of fair value less costs of disposal and value in use.