Recommendation Cash And Equivalents Ifrs Adjustments For Prepaid Expenses

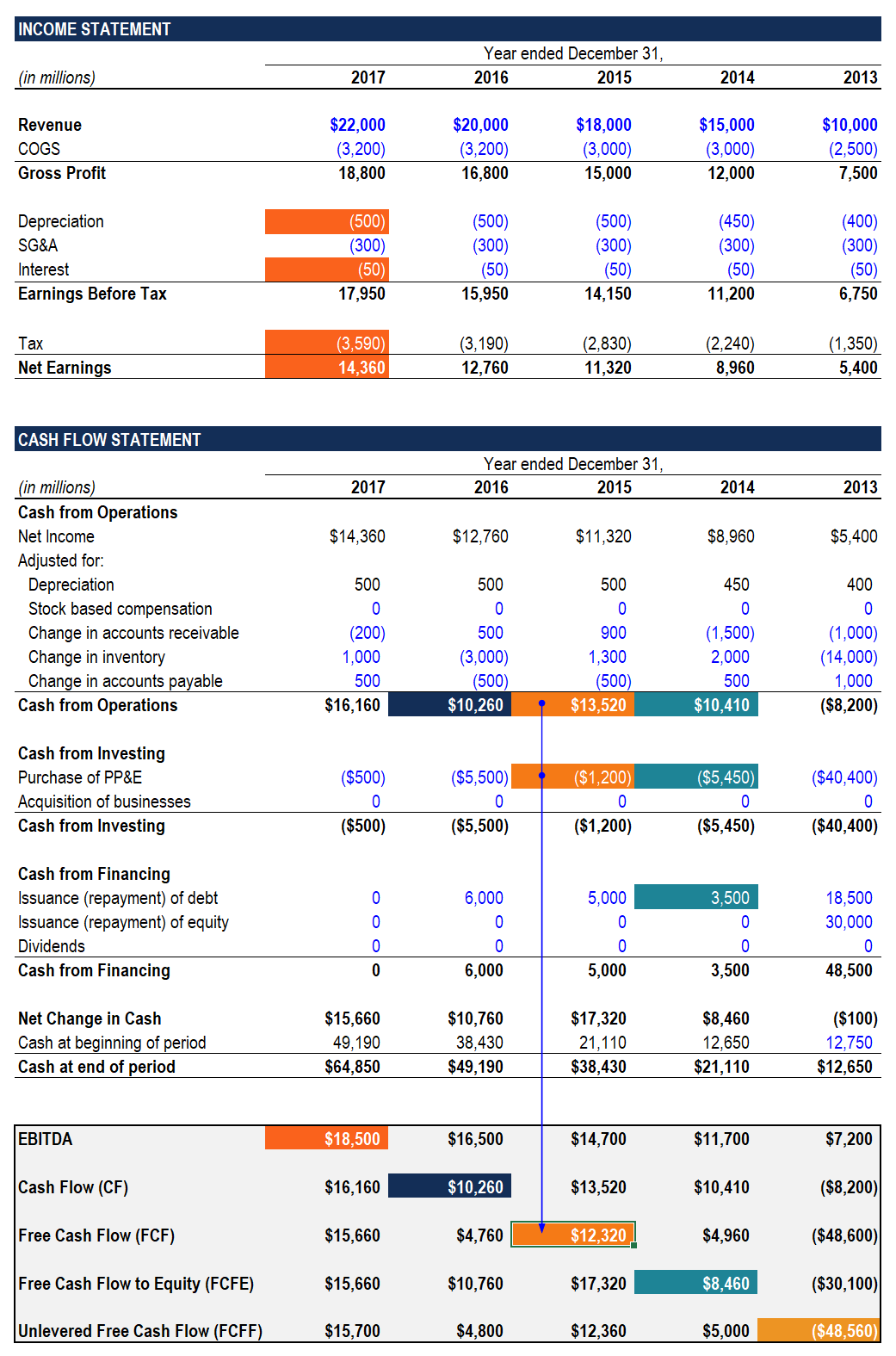

The Ultimate Cash Flow Guide Understand Ebitda Cf Fcf Fcff

These are measured at amortised cost. Cash may be net of bank overdrafts under IFRS Standards. Short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. Included in cash and cash equivalents at December 31 2020 were amounts totalling 65 million 2019. Cash equivalents would include most bank term deposits with a short maturity period and would most likely include government bonds that have around three months or less to maturity at the time of acquisition. The classification and measurement of bonds and other receivables or debt instruments overall is driven by the entitys business model for managing the financial assets and the complexity of the contractual. IFRS 5 Classification in conjunction with a planned IPO but where the prospectus has not been approved by the securities regulator. Subscribers have no page view limit. Cash and cash equivalents Publication date. To view the remainder of this page please register or subscribe.

Consequently the IFRIC decided that it needed to consider whether units in money market funds should be in-substance cash equivalents.

In such cases bank overdrafts are included as a component of cash and cash equivalents meaning that bank overdraft balances would be offset against any positive cash and cash equivalent balances for the purposes of the statement of cash flows. The definitions of these terms are therefore central to its proper preparation. Consequently the IFRIC decided that it needed to consider whether units in money market funds should be in-substance cash equivalents. No specific format is prescribed by the standard but cashflows must be presented under these three main headings. Cash and cash equivalents and debt instruments Measurement of cash and cash equivalents trade receivables and other short-term receivables remains unchanged. See the Proposed amendments that would affect these classifications under IFRS Standards.

In such cases bank overdrafts are included as a component of cash and cash equivalents meaning that bank overdraft balances would be offset against any positive cash and cash equivalent balances for the purposes of the statement of cash flows. Cash and cash equivalents rather than financing cash flows. Included in cash and cash equivalents at December 31 2020 were amounts totalling 65 million 2019. The statement classifies cash flows during a period into cash flows from operating investing and financing activities. Money market funds and reverse repos used in cash management provided higher yields. No specific format is prescribed by the standard but cashflows must be presented under these three main headings. CASH EQUIVALENTS Investment securities that are short-term have high credit quality and are highly liquid. Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value. 03 Apr 2020 ca PwC In depth INT2020-02 IAS 7 defines cash equivalents as short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. In the fact pattern.

On the Balance Sheet cash and cash equivalents comprise cash and shortterm deposits with a maturity date of three months or less held with banks and liquidity funds. 431 million subject to currency controls or other legal restrictions. Cash and cash Equivalents. In the fact pattern. Subscribers have no page view limit. Cash and cash equivalents Publication date. IFRS 5 Classification in conjunction with a planned IPO but where the prospectus has not been approved by the securities regulator. Cash comprises cash on hand and demand deposits. Subscription is 6990 EUR per year. Registered users have up to 20 page views per month at no cost.

At its June 2018 meeting the IFRS Interpretations Committee the Committee discussed the circumstances in which short-term loans and credit facilities may be presented as a component of cash and cash equivalents. Cash equivalents. Cash and cash Equivalents. On the Balance Sheet cash and cash equivalents comprise cash and shortterm deposits with a maturity date of three months or less held with banks and liquidity funds. IFRS 5 Classification in conjunction with a planned IPO but where the prospectus has not been approved by the securities regulator. 03 Apr 2020 ca PwC In depth INT2020-02 IAS 7 defines cash equivalents as short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. Cash equivalents are short-term highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value. The entity has short-term loans and credit facilities. Included in cash and cash equivalents at December 31 2020 were amounts totalling 65 million 2019. The classification and measurement of bonds and other receivables or debt instruments overall is driven by the entitys business model for managing the financial assets and the complexity of the contractual.

The classification and measurement of bonds and other receivables or debt instruments overall is driven by the entitys business model for managing the financial assets and the complexity of the contractual. IAS 76 provides the following definitions. Short-term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. Cash comprises cash on hand and demand deposits. Not under US GAAP. IAS 77 then notes that cash equivalents are held for the purpose of meeting short term cash commitments rather than for investment or other purposes. 431 million subject to currency controls or other legal restrictions. IFRS 5 Classification in conjunction with a planned IPO but where the prospectus has not been approved by the securities regulator. To view the remainder of this page please register or subscribe. In the Statement of Cash Flows cash and cash equivalents also include bank overdrafts which are recorded under current liabilities on the balance sheet.

The IFRIC also decided that the criterion in the definition that cash equivalents must be convertible to known amounts of cash means that the amount of cash that will be received must be known at the time of the initial investment. IAS 76 provides the following definitions. Cash and cash Equivalents. In practice most entities follow this. At its June 2018 meeting the IFRS Interpretations Committee the Committee discussed the circumstances in which short-term loans and credit facilities may be presented as a component of cash and cash equivalents. Cash equivalents. Operating investing and financing. Cash and cash equivalents rather than financing cash flows. 431 million subject to currency controls or other legal restrictions. IAS 7 Identification of cash equivalents.